An Overview of Return on Sales and Operating Margin

Feb 24, 2024 By Triston Martin

Both the ROS and OPM often describe the same financial ratio. Although they are often referred to as the same thing, there is a significant difference. The numerators (top of the equation) distinguish ROS from the operating margin. ROS is based on EBIT while operating margin uses operating income.

Return on Sales

ROS is a measure that evaluates a company's operational efficiency. This indicator shows how much profit is being made per dollar of sales. A rising ROS means a company's efficiency improves, while a falling ROS could indicate financial trouble. ROS closely correlates with a company's operating profit margin.

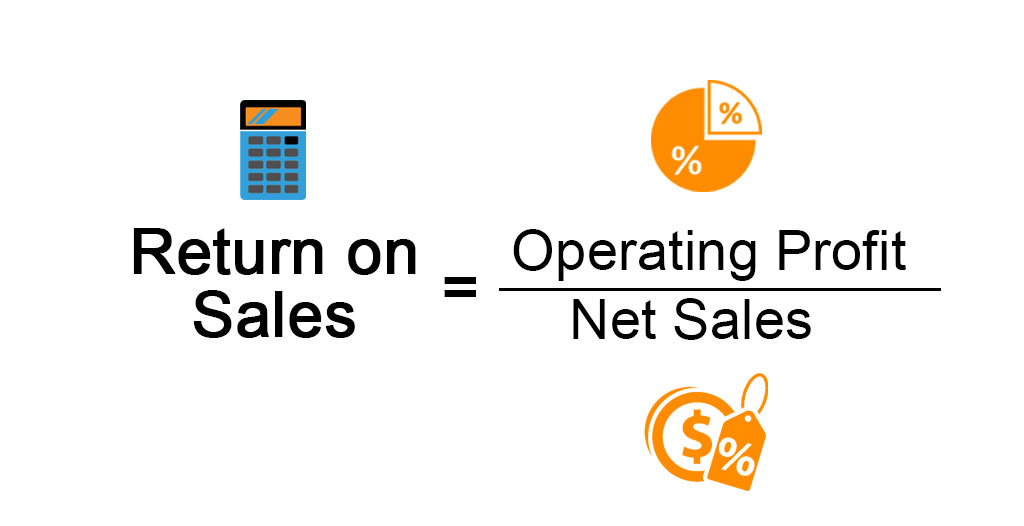

How to Determine Return on Sales

Investors might be surprised to see those different companies report net sales and revenue when calculating the return on sales. Net sales are total revenue less than customers' credits or refunds for merchandise returns. Companies in the retail sector will most likely list net sales, while other companies will list revenue. Here are the steps for calculating return on sales.

It is possible to locate net sales on your income statement. However, it can also be listed under revenue.

On the income statement, locate operating profit. Ensure to exclude non-operating expenses and activities, such as taxes or interest expenses.

Divide the operating profit by a net sale.

The financial ratio of return on sales measures how efficiently a company generates profits from top-line revenues. This ratio measures a company's performance by analyzing the percentage of total revenues that are converted to operating profits. This calculation shows how efficiently a company produces its core products and services and how well its management manages the business. ROS can be used to measure efficiency and profitability. This efficiency ratio is used by investors, creditors, and other debtholders because it accurately indicates the percentage of operating cash a company makes from its revenue.

ROS can be used to compare calculations for current periods with those from past periods. This allows companies to perform trend analyses and evaluate their internal efficiency over time. It's also possible to compare the ROS percentage of one company with that of another, regardless of their scale.

This allows you to compare the performance of small companies with Fortune 500 companies. ROS should not be used to compare companies in the same industry, as ROS can vary widely across industries. For example, a grocery store has lower margins and a lower ROS than a technology company.

A similar financial ratio is often described by operating profit margin and return on sales. The difference in how each formula is calculated is the main difference. The operating margin formula is written as operating income divided by net sales. This is the standard way to write it. The return on sales formula is very similar, except that the numerator is often written as EBIT, while the denominator remains net sales.

Limitations

Only compare companies in the same industry and, ideally, among those with similar business models and annual sales figures should you use return on sales to compare them. Comparing companies in different industries that have drastically different business models can lead to confusing results.

Operating Margin

There is a lot of overlap between the ROS and the operating margin. The operational margin may be calculated by dividing the operating income by sales. A similar concept to ROS, the operational margin represents the company's net operating profit as a percentage of each dollar of sales. The relationship between operating income and other operational efficiency indicators is similar to that of EBIT. Similar to operating income is the concept of operating cash flow. While operational income takes into account depreciation, operating cash flows take these and other non-monetary variables into account.

The Key Differences

Analysts, lenders, investors, and analysts use ROS to compare different capital structures within different industries. These metrics do not take into consideration how businesses obtain their financing. A high ROS, or operating margins, could indicate an increased risk to the business. Higher ratios indicate that the company is profitable and can generate profits from sales.

EBIT versus operating revenue is the major difference between these ratios. ROS uses EBIT, which is not a Generally Accepted Accounting Principles measure (GAAP). Operating income is a GAAP measure. The operating margin is calculated using the operating margin. EBIT permits adjustments and allowances that GAAP doesn't allow in operating income. Operating income may not be comparable to GAAP for certain measures, such as non-recurring revenue or expenses.

Non-recurring expenses are expenses that won't happen again. These include those incurred in mergers and acquisitions and when purchasing real estate or equipment. Gains on asset sales or insurance settlements can also be considered non-recurring income. Extraordinary income can also be considered non-recurring income.

Navigating Money Transfer Regulations: Ensuring Your Financial Safety

The Best Stocks To Buy In Semiconductors

A Brief Overview and Introduction to Momentum Trading

Best Day Trading Oscillators

Comprehensive 2024 Review of Gold Gate Capital: Features, Pros, and Cons

Understanding Loan Stacking in Commercial Lending

Essential Questions to Ask a Mortgage Lender

FedNow and RTP: A Close Market in Instant Payment Adoption

How to Create a Facebook Business Page: Easy 6-Step Guide